The Main Objective: Risk Management

Markets closed last week with an improved risk profile—but that will be put to the test as geopolitical developments over the weekend flow into the futures open and, more critically, the Monday session and week ahead. Historically, my review of market performance around war-related events shows that the first 1–2 weeks often see downside volatility, but one-month returns tend to skew positive. The setup points to near-term turbulence.

I won’t attempt to forecast the sequence of geopolitical events or their long-term impact. When it comes to managing my book, I let the data and price action dictate when to flip the switch to a defensive posture. The priority is always risk management—preserving capital and protecting gains. The last full alarm was triggered on February 21. What followed was a 19%+ drop in the S&P 500 over the next month. That signal proved timely—a reminder that while not every alarm leads to a major drawdown, it’s the ones that do that matter most.

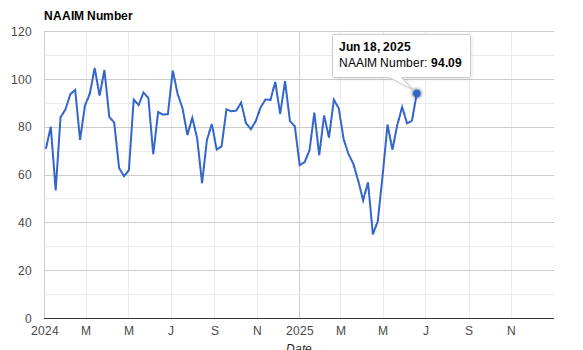

At the low of that correction, the Sunday note called out record low sentiment and reduced US equity exposure—key ingredients for a bounce. Now, we're seeing the mirror image on positioning: equity exposure via the NAAIM Index is back at annual highs. That’s notable, especially with the S&P 500 still just shy of all-time highs.

Sentiment, meanwhile, has cooled into a more neutral range. Geopolitical headlines have helped tamp down enthusiasm. From a bullish perspective, that mismatch—strong positioning but subdued sentiment—can be fuel for the next leg higher.

Subscribe to stay informed. Get updates every Wednesday and Sunday with clear, risk-managed perspectives on where the market stands—and where it might go next.